Chapter 1 — The Basics

Mortgage Application Steps and Timeline

The timeline for applying for a mortgage starts when you’ve decided you’re in the market for a new home. Below are the general steps for getting a mortgage - we’ll go into more detail later, but figured an overview would be a good place to start!

1. During Home Search

- Find a lender

- Determine how much you should borrow

- Decide what loan program(s) are best for you

- Gather documents

- Obtain pre-qualification letter

2. When You Find a Home

- Obtain pre-approval letter

- Submit an offer

- Perform home inspection

- Negotiate your contract

- Rate lock

3. After Signing Contract

- Meet loan processor

- Receive, review, and sign loan disclosures

- Provide all documentation required for loan

- Pay option and earnest money

- Get appraisal

- Schedule date and time for closing

4. Closing the Deal

- Pay closing costs

- Sign papers

- Distribute funds to seller

- Get keys, move in!

Mortgages Explained Like You’re Five

A mortgage is just a special kind of loan, where the house is the collateral, or the security for the loan, which means if you (as the borrower) don’t pay the loan, the lender will take the house. While you do get to live in the house and use it as if you owned it in every respect, the bank / lender actually holds the title to the house until you pay off the loan.

Basic Terminology (Down Payment, Principal, Interest, and Equity)

The reality of home ownership is not cut and dry, so let’s use an example to help you understand the concept of Equity.

Let’s say you want to buy a house that is priced at $500,000. You have saved up $100,000, and will use that as a down payment on the house. So you still need $400,000 to make up the difference.

You go to your local bank, and get a loan for $400,000, and the bank sets the interest rate at 5% (we'll discuss how the bank determines your mortgage rate shortly). This interest rate is annual, so on each monthly mortgage payment, you will only pay 1/12 of the interest rate, which in this case is about 0.42%, in addition to the Principal.

Let’s assume this loan is a standard, fixed rate mortgage (adjustable rate mortgages are covered in more detail here). This means the 5% rate of interest will never change for the entire Term of the loan. The Term is the length of the loan, or how long the bank gives you to pay the loan back. The standard term for a mortgage loan is 30 years, so let’s go with that for our example.

Now you’ve got the $400,000 loan from the bank, and along with the $100,000 you used as a down payment, you purchase the house. Now the house is your asset. However, as we’ve discussed, you don’t own the house completely, since the bank holds the title. The $500,000 asset you have just acquired has a $400,000 liability, in the form of the mortgage loan. You now have $100,000 equity in the $500,000 house.

Equity is simply the value of the asset, minus the value of any liabilities, which in this case is the the $400,000 loan. As the market value of the house changes, and as you pay off your loan, the amount of equity you own in the house will also change. Assuming the price or market value of the house remains at $500,000, your equity will increase as you pay off the debt. Eventually, once you pay off the entire loan, you will have 100% equity in the house.

How To Calculate Mortgage Payments

The monthly payments of principal plus interest are based on the amount of the loan, rather than the value of the house. For a fixed rate mortgage, each payment will be exactly the same for the life of the loan. However, the portion of the payment that is interest will continually decrease, until the final payment, which will be entirely principal.

Let’s go back to our example to see how this works. Before the 30-year term of the loan begins, you borrow $400,000, and each month you have have to pay 0.42% interest, in addition to the principal. So by the end of the first month, with the 0.42% interest accrued, the loan balance will now be $401,680.00. This is because over the course of the first month, 0.42% of $400,000, in the form of accrued interest, was added to the loan balance.

Each payment over the life of the loan will be roughly $2,147.29. Since $1,680.00 was added to the loan balance during the first month, only $467.29 of your first payment will go towards paying back the Principal, and the remainder, $1,680.00 will only pay back the interest of the loan.

$467.29 may seem like very little, but as you pay down the principal, the portion of your monthly payment that is interest will continually decrease. In our example, after the first month’s payment, the loan balance will be reduced from $401,680.00 to $399,532.71. So, for the second month, the 0.42% interest will accrue on $399,532.71, rather than $400,000.

The portion of your $2,147.29 monthly payment that is only interest will decrease each month, until the final month, when your payment will be all Principal, and the loan will be paid off, giving you 100% equity in your home.

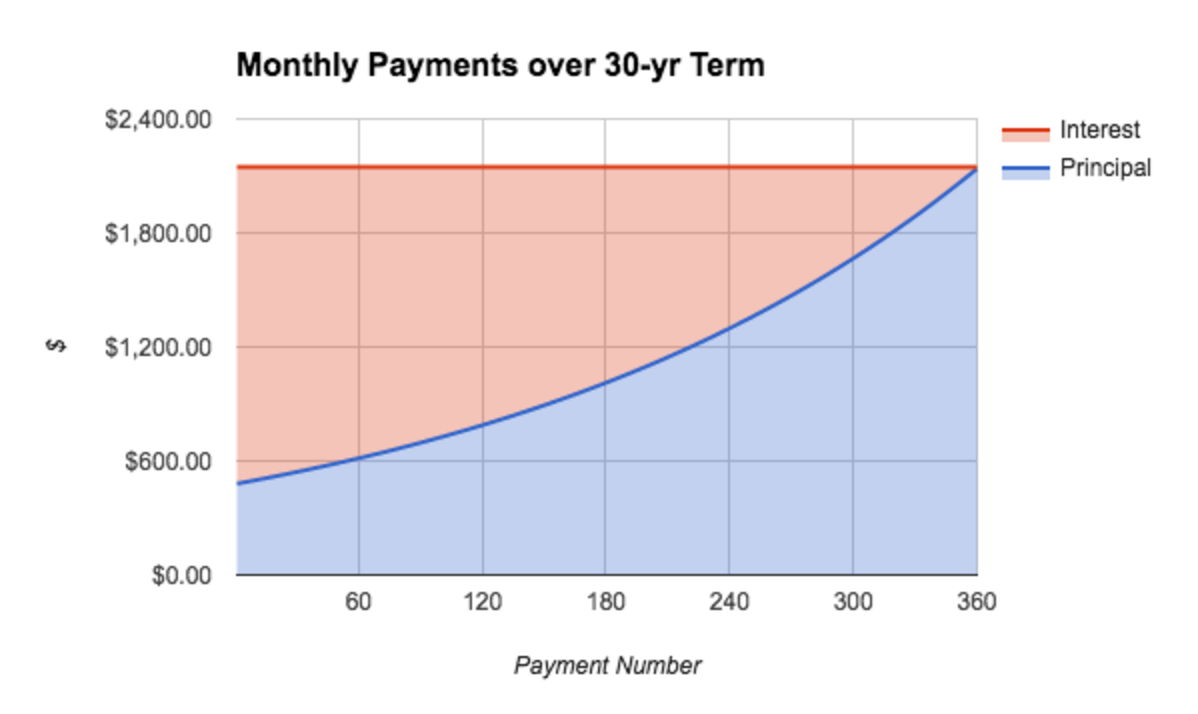

The chart above shows how the distribution of principal and interest works for our example of a $400,000, 30-year, fixed rate mortgage. As you can see, the portion of each payment that is interest (red) decreases, while the principal payment (blue) increases, adding up to the same total of $2,147.29 for each payment. This chart shows the entire 30-year term of the loan. The blue portion will increase until the last payment where the entire payment will be principal, and once that final payment is made, the entire loan will be paid off, the borrower will have 100% equity in the property.

The Cost of Borrowing

Origination Fees

Whenever a borrower applies for a loan, there are certain costs associated with the application process, whether or not they ultimately get the loan.

Once the borrower submits the information about his or her credit, income, and anything else the bank may require, the bank uses this information to underwrite the loan. Underwriting is just a term for a financial analysis of the particular borrower, and whether or not they can afford to take on the loan.

Origination fees are generally broken down into mortgage points, or discount points, and as discussed in the next section entitled Factors Affecting Mortgage Rates, these are fees paid upfront that will decrease the interest rate, in addition to covering the costs of origination. One point is equal to 1% of the total loan, so in our example of a $400,000 loan, each point would equal $4,000.

Disclaimer:

The materials provided are for informational purposes only and is presented without warranty. It is not financial or legal advice and use of the information is at your own risk. To the maximum extent allowed by law, InvestmentZen disclaims any and all liability in the event any information, commentary, analysis, opinion, advice and/or recommendations prove to be inaccurate, incomplete, or unreliable. You should consult with a professional and do your own due diligence before making any financial decisions.